Initial Public Offerings (IPOs) are riding high right now.

You might’ve heard about the Snowflake IPO making headlines.

It’s a company with a special type of deal structure that most investors might not have heard of before.

Leading the charge and fury in the IPO markets are SPACs, (Special Purpose Acquisition Companies).

SPACs start as a shell company and sell shares to investors. It doesn’t have any operations or business of its own. The purpose is to acquire one that does.

It’s like a backdoor route for large sums of money (think $100 million, or more) to get into the stock market.

Investors and the private equity funds behind these SPACs love it, because there is much less underwriting, and the paper pushing process through the SEC is easier.

Much like private placements in the red-hot mining space–which we’ll get to in a moment–SPACs have rules.

- SPAC’s have a deadline of 24 months to acquire a business.

- If they don’t, investors get their money back with interest.

- You can also request your money back if you don’t like the acquisition.

However, you can make money with SPACs–and quickly.

Anyone that invested in the VectoIQ SPAC before or during its acquisition of Nikola Motors (NKLA) could have made 10x returns.

We recently alerted subscribers to a SPAC in the Katusa’s Resource Opportunities newsletter portfolio.

It’s been up by as much as 30% since the first research report.

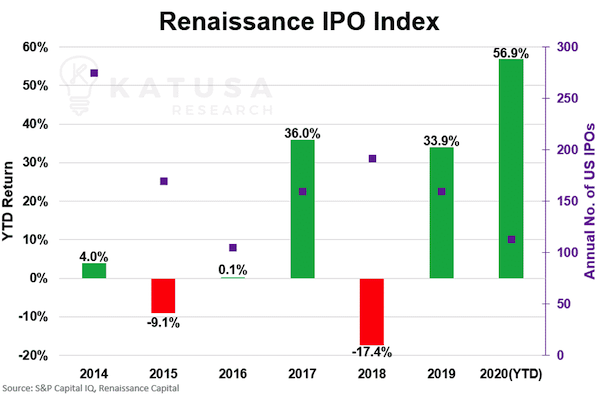

With all the headlines, we could expect that IPOs will flood the market.

In fact, in the next chart you’ll see that YTD in 2020 we’ve seen the 2nd lowest number of IPOs (113) in 6 years.

But the return of those IPOs through the lens of the Renaissance IPO index is much higher than the last 6 years.

What Happens When New Paper Shares are Created?

Capital flows are one of the least understood, most closely guarded secrets in the resource sector.

Bull and bear markets are driven by expansions and contractions in capital flows.

This capital comes from everyone—retail investors all the way to trillion-dollar sovereign wealth funds.

Knowing how to profit from these tidal changes in the market is incredibly important for the contrarian investor.

We have all heard a few marquee lines related to trading:

- “Buy when there’s blood in the streets.”

- “The market can stay irrational longer than you can stay solvent.”

- “You know it’s time to sell when shoeshine boys give you stock tips.”

I want to talk about the last one…

Being a good seller is as important as being a good buyer and stock picker.

Realizing a profit is important, but selling is a lot more than placing a market sell order for your entire position and moving on.

Selling should be just like an alligator: Slow. Methodical. Strategic.

Always use limit orders.

Let the buyers come to you.

Discipline is required, when buying and selling shares.

And here’s why…

How to Prepare for Amateur Hour…

I want to use my points above to help you understand how fund managers (who get redemptions) and amateur investors sell and put pressure on a stock.

My expertise is in finding and getting myself and my subscribers into resource deals in gold, oil, copper, uranium and silver.

We are coming into the last few months of a year—that has seen share prices of good and bad gold deals soar because of the rise in the gold price.

Throw in a U.S. Presidential election… I believe we are going to see pressure on many resource stocks.

Now, this could be a major opportunity for us.

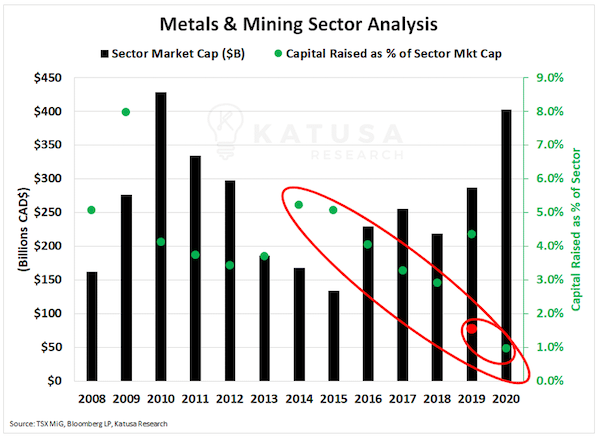

Let’s start with how much capital has been raised in the metals and mining sector.

Last year, we saw equity financings rise above CAD$12 billion for the sector—a value not seen since the last run up from 2009–2011.

2019’s spike was due in large part to Katanga Mining’s CAD$7.6 billion rights offering.

If you remove that…

Equity financings totaled just CAD$4.9 billion, which would make 2019 the worst year since 2008 when the TSX began releasing statistics.

It was a very tough year for many companies.

2020 will be an improvement. Gold has performed well, and financings are already approaching CAD$4 billion.

What’s more important is what these financings represented versus the sector’s market capitalization.

How Much Money Really Went into the Precious Metals Sector?

In the next chart, you will see equity financings as a percentage of sector market capitalization.

Historically, financings represented between 3.5% and up to 8% of the sector’s market capitalization. Over the last 5 years, financings have cratered.

Again, if you remove Katanga’s rights offering, financings in 2019 would have represented just 1.7% of the sector’s market cap (red dot).

Even with the precious metals market rocking, so far in 2020, financings have represented just 1% of the sector’s market cap—the lowest representation since at least 2008.

For the last 7 years, the trend has clearly been toward less capital going to work, regardless of sector performance.

This means that although mining stock prices are rising, financings are not increasing at the same rate.

You can attribute this trend to 3 different factors:

- Prices are rising faster than financings are happening. That is not the case when compared to previous cycles.

- The bigger funds and the generalist funds have not yet gotten into the mining financings like they have in the past.

- Passive funds are focusing on ETFs rather than on equities.

Number 3 is where I believe the significant change is.

But with all the new IPO, listings, financings, deals that are hitting the markets, what happens to all those new shares once they start trading?

The Great Flood: Free Trading Stock Will Flood the Market This Fall

We are data nerds. We compile incredible amounts of data that others do not.

Scouring through our two best data terminals along with the TSX financing data, we have compiled a chart you won’t see anywhere else.

Ironically if you used each data terminal individually you would get three different numbers for financings this year and every other year.

As you know, a large portion of equity financings are conducted through private placements.

Shares in those financings are restricted for 120 days after the close.

It is only under an IPO or short-form prospectus financing that there is no four-month hold.

Once the 120 days are up, the shares become unrestricted and investors in the private placement are free to sell their shares.

For every seller of shares, there needs to be a buyer.

It’s not rocket science to expect that the stocks that have financings coming “free trading”, will trade lower.

The expiration of the restrictions can create significant selling pressure as investors look to recoup their capital—all at the same time.

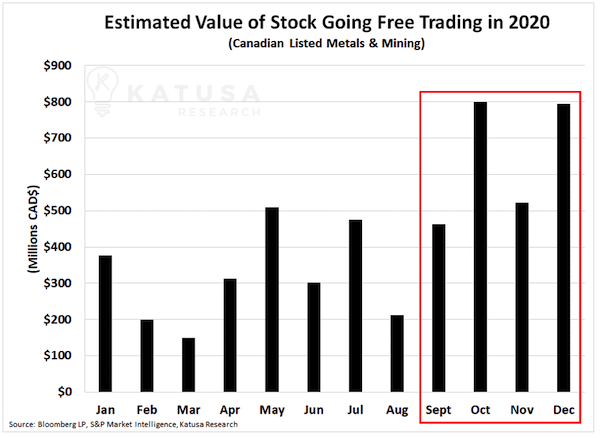

The Gold and Silver Paper Wall

You’ll want to pay attention to this.

The chart below combines the data sets and encompasses 95%+ of the equity financings in the last 12 months—any equity financing over CAD$5 million.

From this new data set, we’ve calculated the dollar amount of upcoming free trading stock.

So, beware.

This is where the flood of paper will enter the market…

You’ll see that the next few months have significantly more free trading stock than the previous 8 months.

In fact…

I estimate over CAD$2.5 billion worth of mining sector stock will go free trading over the next few months on the TSX and TSX-V exchanges.

The majority are gold and silver stocks.

This is an enormous amount of capital for the mining sector to be able to absorb.

To put it in perspective…

If I do not want to disrupt normal trading activity, it can take many days or months for me to close positions worth 7 figures.

Now extrapolate my situation to the entire market and it’s CAD$2.5 billion dollars which is coming free trading.

This creates a serious problem for relatively illiquid listed mining companies.

I highly doubt there is CAD$3-4 billion in new capital ready to step in and absorb those shares in the open market at the current prices—which are much higher than the financing prices.

A Real-Life Example

Here’s a real-life example of a situation likely to experience major havoc sometime this fall:

A small junior whose management team I have never heard of and that has never been involved in mining before raised $2 million in May.

Share prices since the private placement are up 800%, not including the warrants. The company trades 225,000 shares a day right now.

The private placement was for just under 30 million shares. Again, the math doesn’t lie. Converting “paper” profits to realized profits will be nearly impossible for those investors.

The list of these types of deals is pages long.

Most of the companies are doing financings to keep the lights on or to fund a promotion or to raise the price higher so they can unload stock.

I’ve always avoided those types of pie-in-the-sky burning matches and I’ll continue to avoid them for the rest of my career.

The risk/reward is horrible.

However, many good companies also financed earlier this year. And most certainly there will be investors looking to recoup some principal.

In the event of a sudden selloff or a few bad days in the gold market, it can provide us alligators with MAJOR opportunities.

And we’ve run the numbers on a handful of companies we want to own. They are on our alligator watchlist.

As the newly created shares come free trading, there will be pressure on many gold and silver stocks.

Prepare for that opportunity well before it comes.

It could be your last ticket to pick up shares of great gold and silver stocks, on the cheap.

Editor’s Note: Doug Casey and Marin Katusa just released an urgent video which outlines exactly how they’re positioned to profit from this rare opportunity.

They discuss how this situation has played out numerous times and why even a small amount of money put into the right mining stocks today could deliver life-changing rewards. Click here to watch it now and see how you could join them in making enormous profits.

Source: https://internationalman.com/articles/what-happens-when-hot-ipos-financings-hit-the-market-gold/